Technology

Basis Platform

Advertising Operating System

Communication Portal

Intelligent Collaboration

All Channel Activation

Activate Media on Every Channel

Consulting

Resources

Grace Briscoe is SVP of Candidates and Causes at Basis Technologies

Digital advertising spend soared even higher for the 2022 US elections. This seemed like an aberration because of the record-setting 2020 US elections that generated the highest voter turnout ever. One could reasonably assume that the 2022 Midterms would not generate the same level of marketing as the previous cycle that featured presidential candidates at the top of the ticket. Yet, there was cautious optimism for ad dollars flowing into the market.

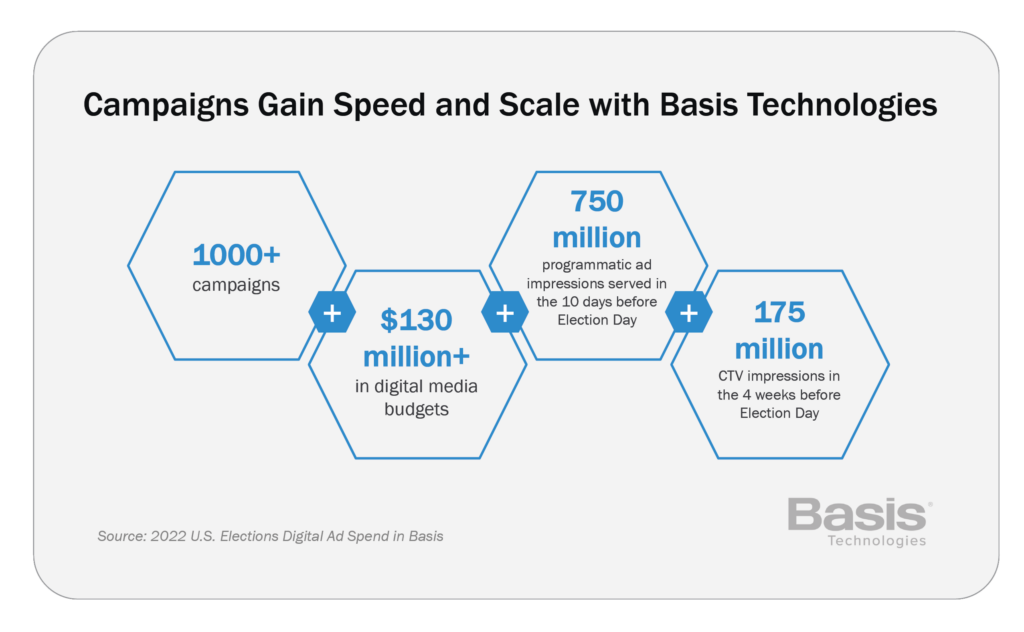

In 2022, more than 1,000 campaigns for state, local and national races managed their digital ad buying through Basis Technologies’ workflow automation and business intelligence platform, Basis, encompassing more than $130 million in political ad spend across video, display, native, audio, and text ads.

Basis Technologies has been trusted by agencies and consultants in politics, public affairs, and advocacy for 15 years. We’ve worked with candidates and advocacy groups at all levels, from Presidential to local elections. This experience gives our team a diversified view on how digital media is being utilized in political marketing.

This is the third research report Basis Technologies has published on the US elections and digital ad spending. Our 2020 report confirmed the growing use of programmatic advertising and the emerging interest in CTV ads, seemingly giving a 2022 winning playbook for midterm campaigns. The marketers followed through, perhaps at the cost of other tried and true tactics.

Could 2024 see the same rate of growth in CTV ad spending? It will likely depend on how inventory availability in programmatic (guaranteed, private marketplace or open bidding) affects tactical decisions. And as ad targeting restrictions based on consumer privacy begin taking effect (on top of Google deprecating third-party cookies in Chrome in 2024), common tactics to identify voters could be constrained. Luckily, political advertisers have long been comfortable with uncertainty.

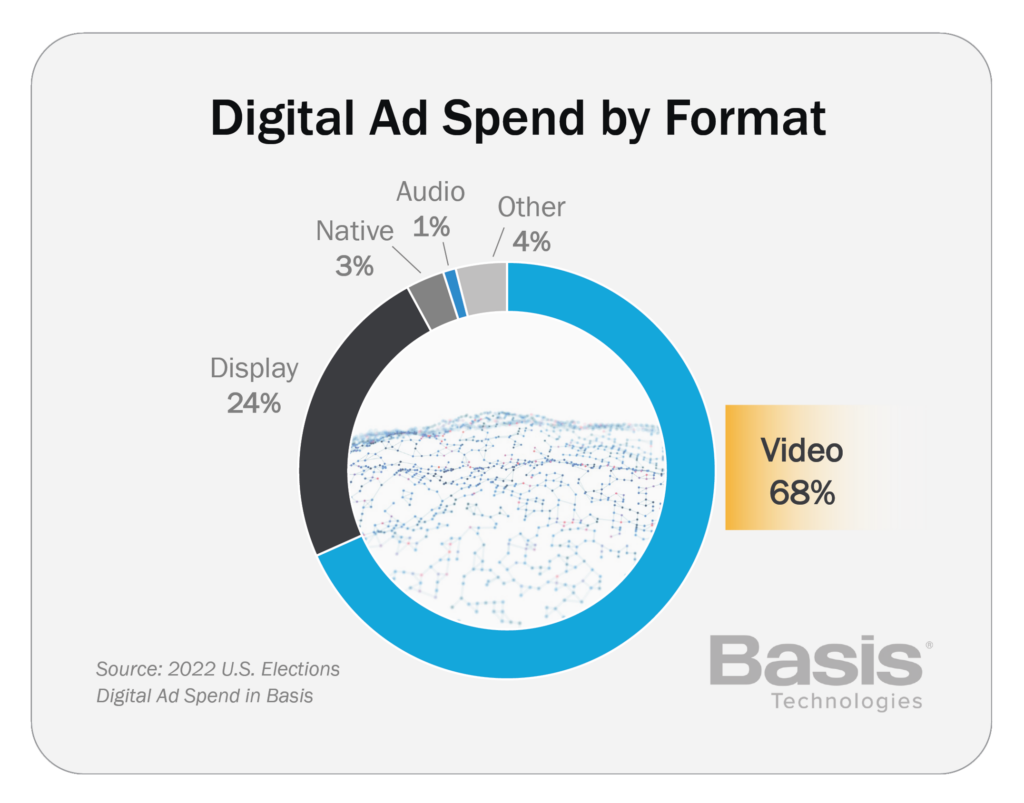

Video ads, whether linear TV or digital formats, have long been popular for political marketers. When we began tracking this data in 2018, video already comprised a majority of ad spend – and that was a time when CTV ad opportunities were nascent. Now that the CTV train is rolling, we can expect continued dominance of video ad spend — the question is how much more can political marketers spend in this format. Much of CTV growth came from video ad dollars previously being spent on desktop. The redistribution in device spend did not necessarily boost format spend for video. There is finite high-quality video inventory now, but publishers could expand video offerings just in time for 2024, when a presidential contest could mean a bigger boost in ad sales than in a midterm.

Other formats should be monitored, especially audio. Native, audio, and others combined had miniscule volume in 2018 (4%) and 2020 (3%). But 100% growth is intriguing, and we believe a significant part was driven by Spotify allowing political ads for the midterms (it did not allow this in 2020). As digital audio and broadcast radio ad inventory become available via programmatic channels, this category could be poised for growth in 2024.

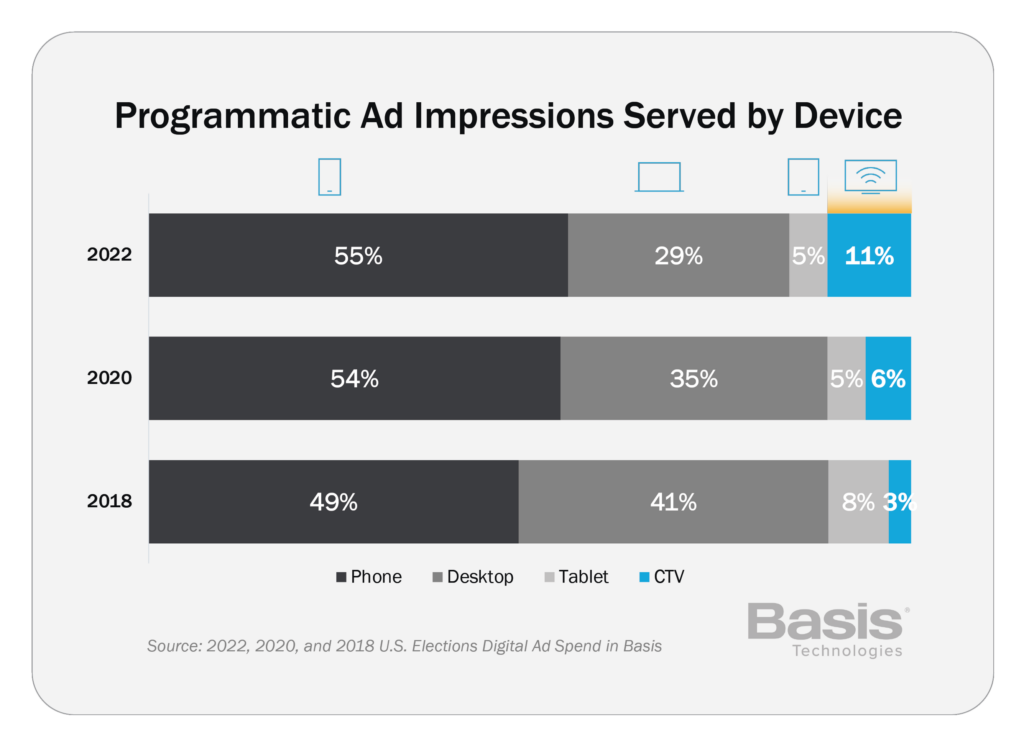

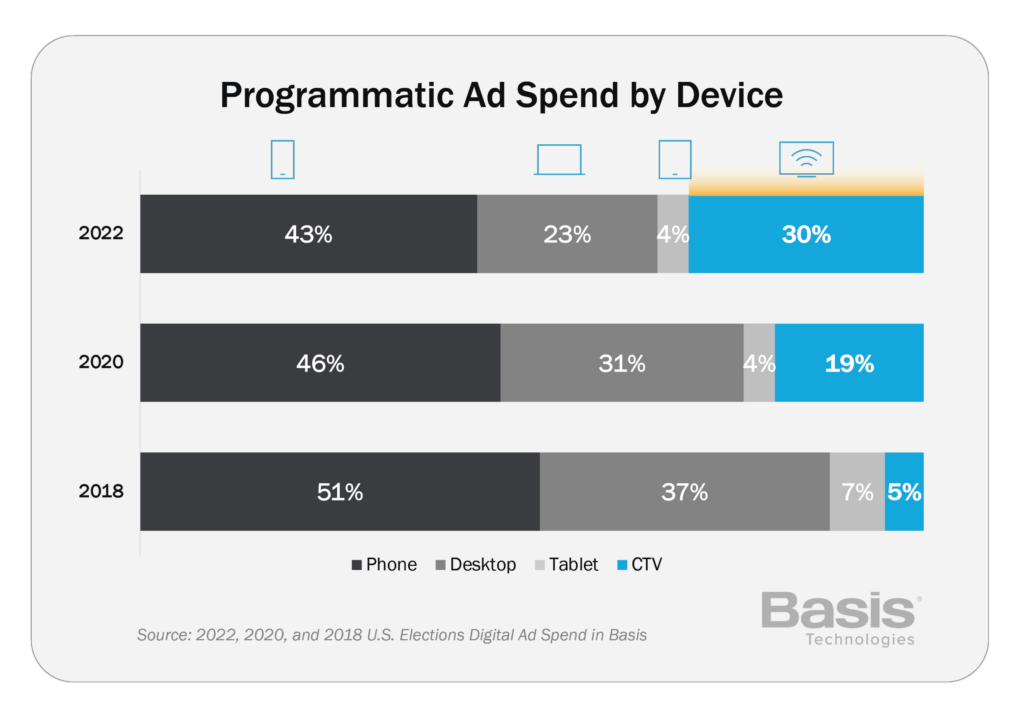

Even though CTV had a significant impact in shifting the media spend by device in programmatic channels, its effect was even greater for direct buying methods. For many inventory suppliers, CTV ad opportunities were primarily available via direct channels. CTV ads was almost half of direct spending for 2022 political marketers. This could be contributing to the decline in social advertising share over the past elections. However, the major social media ad vendors have also implemented restrictive policies for political advertising, in addition to having younger audiences (who are low-propensity voters).

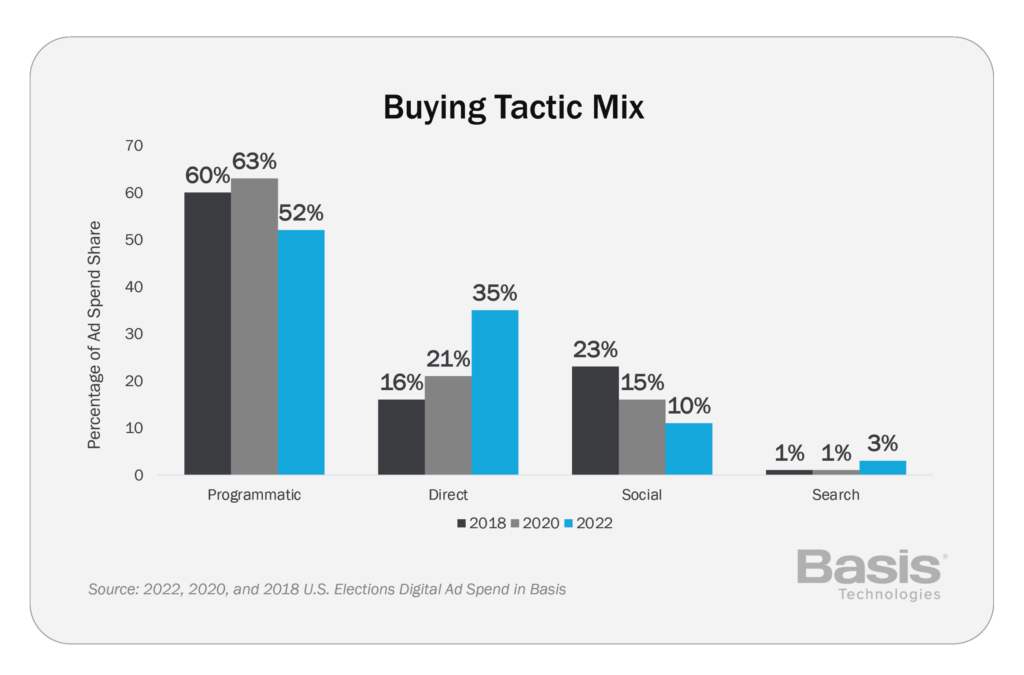

Although programmatic advertising is still the most popular buying tactic, its decline in share in 2022 was unexpected. Nevertheless, programmatic channels experienced strong growth on ads served to CTV channels in impressions and, more so, in spend (67% growth from 2020 to 2022). Private marketplaces are favorite tactics, and we anticipate that increased adoption of programmatic guaranteed as a buying methodology to secure reserved inventory is likely to reverse the curve toward direct IOs. The primary loser in this evolution is desktop ads. While share in mobile ad spend declined somewhat from 2020 to 2022 (it was still steady in impression count between the two cycles), desktop impression and spend share took major hits.

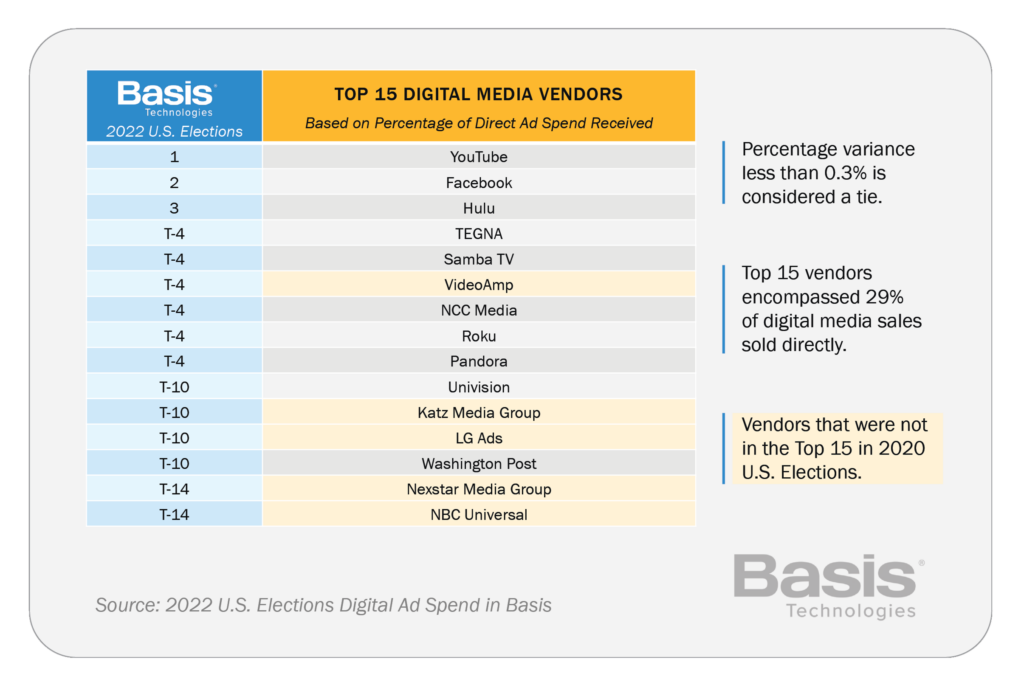

Direct buying was lifted by the demand for CTV inventory. Our report tracks the vendors that received the most ad spend via direct channels (agency or political campaigns transacting an IO with vendors directly). This report has tracked the top 15 vendors in this category of buying, and the past two cycles have displayed the rapid rise of CTV advertising.

Traditional media brands CNN, Fox News, New York Times and Politico, known for politics, were knocked out of the 2022 top 15. These shifts speak to the need for stronger ad options specific for CTV at scale that can lure advertisers from the ease and efficiency of programmatic.

Overall total share of the top 15 vendors declined, going from 38% (2018) to 36% (2020) to 29% (2022).

The top three vendors had 28% in 2018, but now sit at 16% share of direct spend share in 2022. Notably, OTT/CTV vendors went from 4% (2018) to 14% (2020) to 16% (2022). More spend may be going to the long tail, and the duopoly dominance appears to be weakening. The development to watch in 2024 is Twitter, which will allow political ads for the first time since 2019.

Samba TV continued to rise, likely because of advertiser interest in automatic content recognition targeting. New to the list, VideoAmp’s presence also speaks to the importance of CTV planning and measurement tools. Pandora’s consistency for the past three cycles shows it remains the top source for streaming audio. Operational execution and inventory exclusivity make a big different in securing direct ad buys. As 2024 rolls around, the strength of direct buying could be affected as programmatic channels continue to develop better tools in frequency capping and measurement.

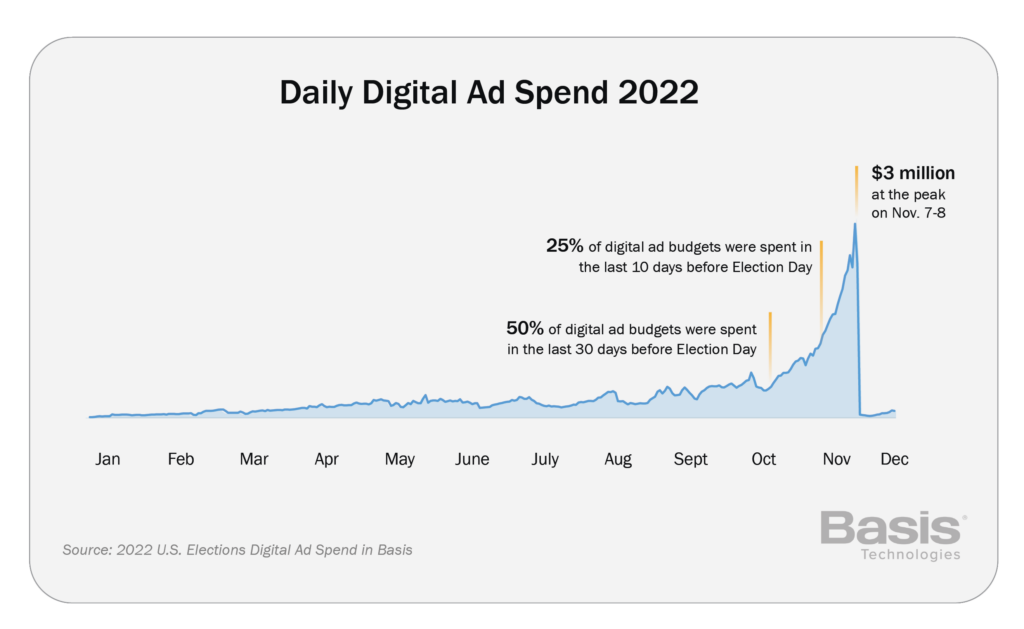

Political ad spending throughout the Midterm election year followed the same pattern as previous election cycles. Half of budgets are spent in the last 30 days before election day for persuasion and early voting and 25% is spent on the last ten days to get out the vote. This is the pattern for cycle upon cycle. The delay in congressional mapping and redistricting had little effect in the overall trend. A few factors that could affect this in 2024 are the presidential primaries and additional runoffs. Even though the country seems a little bit more energized for presidential elections than for midterms, savvy political marketers know that urging turnout and influencing down-ballot votes is still a monumental task.

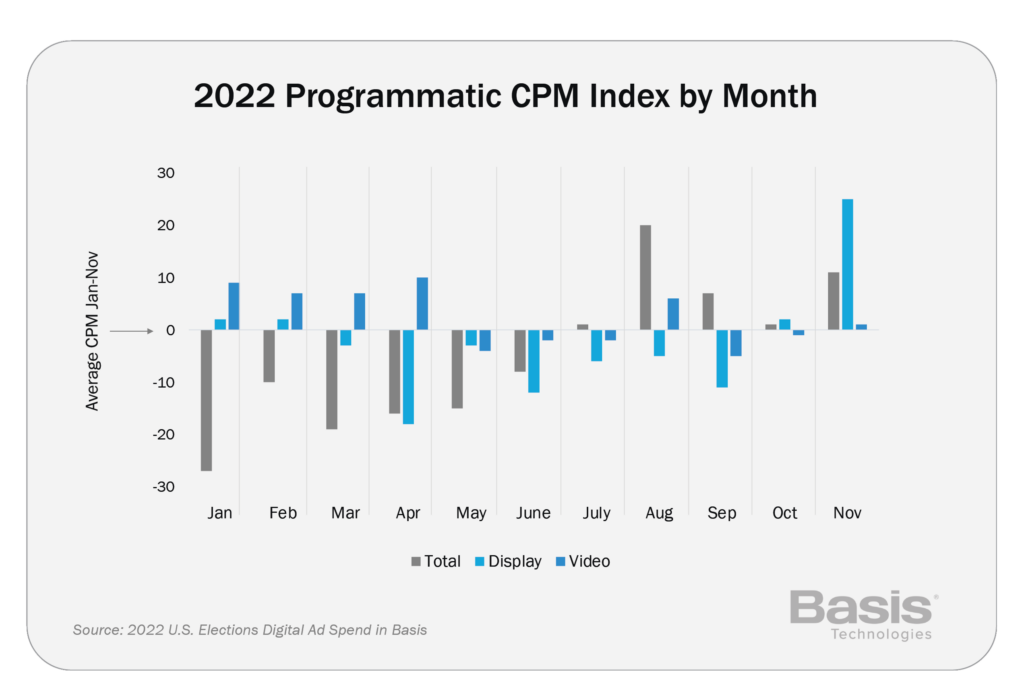

Our programmatic CPM index compares the average pricing per month to the average CPM for the whole election cycle for political marketers. The significant price difference between January and November was driven by ad formats purchased, rather than factors concerning demand and supply. Video made up the majority (74%) of programmatic spend. While video CPMs remained steady throughout the cycle (we saw a variation of less than $1.50), the increased volume of spending on video from August to November at the higher base CPMs commanded by video was the driver of the overall increase. Display totals did also show significant inflation in the days leading up to the election. Although not published in this report because of its marginal impact within overall spend, native ad formats experienced the largest change in CPMs, which averaged over 140% higher in November than in January.

When all buyers are saving budgets for the end, there’s little opportunity to capitalize on lower pricing in the summer months. This pattern should urge advertisers to lock in favorable pricing negotiated in advance through programmatic guaranteed, private marketplaces, or even simple direct buys with vendors.

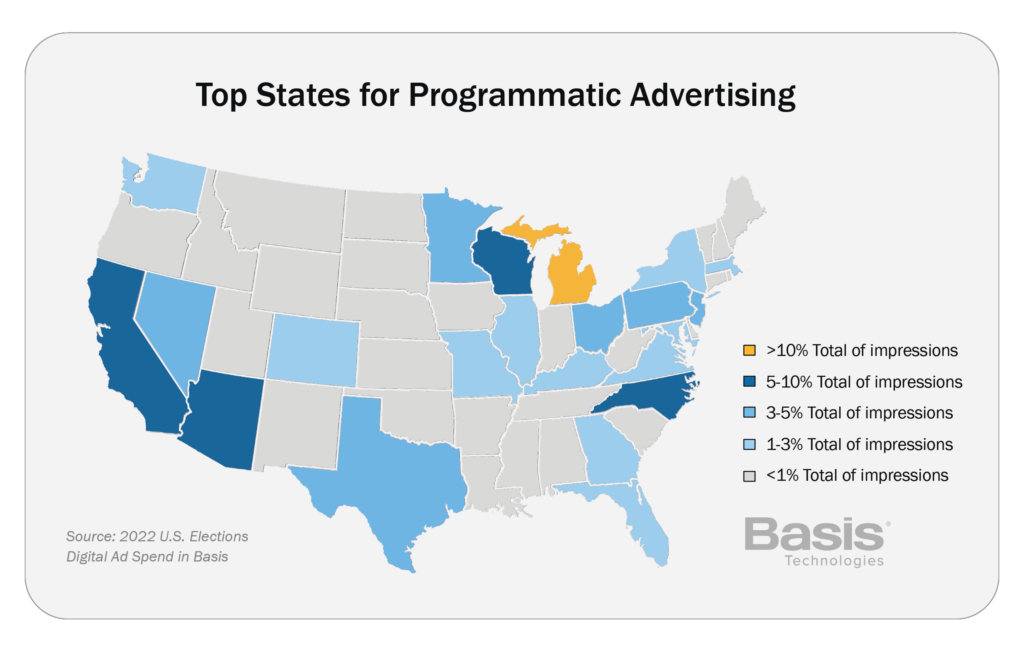

Michiganders were the clear winner (or loser?) during the midterms, receiving the most programmatic ad impressions. People in other large, populous states such as California, Texas, Pennsylvania and Ohio also saw the most ads in terms of impressions and spend. The numerous congressional and state senate seats, and their competitiveness, in these areas are contributing factors for driving ad serving. Beyond the top 11, a large majority of states received 2% or less in total ad impressions in 2022, including Illinois (1.76% impressions share). These numbers could change dramatically when the electoral college is a factor in 2024.

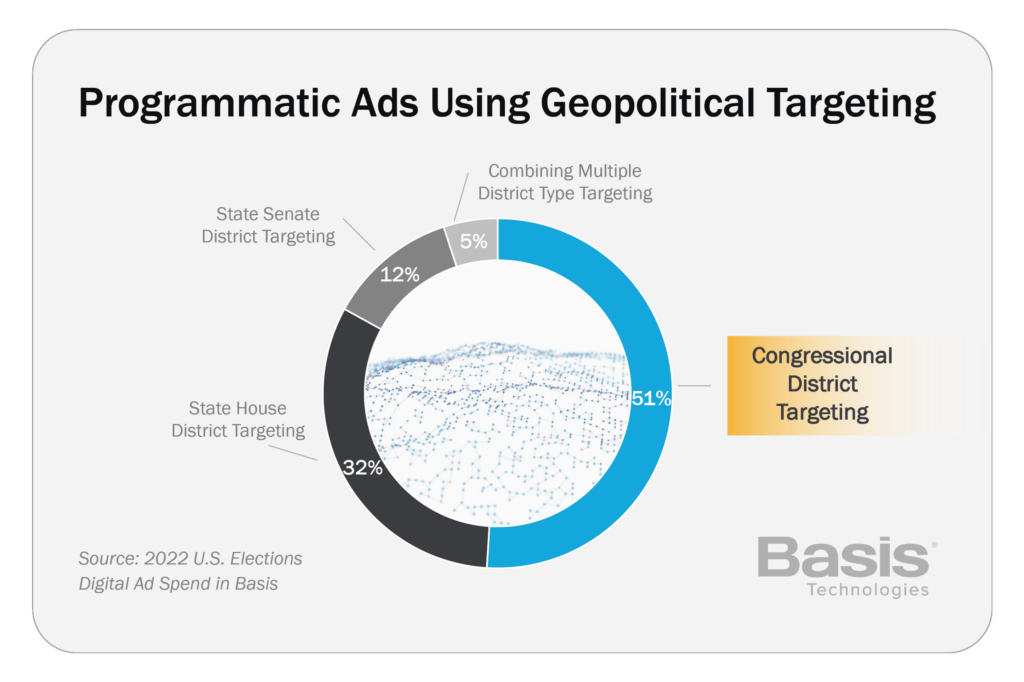

Almost 20% of political programmatic ads used geopolitical targeting, where advertisers select specific districts to target. The most popular among these tactics is Congressional District Targeting, likely as a factor of the larger districts. Frequent updating of geopolitical districts throughout the chaotic redistricting process was key to the effectiveness of this targeting.

When Google blocks third-party cookies on Chrome, it could trigger political marketers that were heavily reliant on cookie-based tactics to move more spend into other tactics. As these marketers grow more familiar with these tactics (State Legislative District Targeting just debuted in 2022), they may decide that 2024 is the right time to transform their campaigns to these forms of finding voters.

CTV advertising was the dominant story in nearly every aspect of the 2022 midterm elections. More than 750 million programmatic ad impressions were served in the final 10 days and 175 million CTV impressions in the final four weeks.

Political marketers are sharpening strategies and tactics heading into 2024. Premium guaranteed placements, procured through direct buys, are key despite the ongoing popularity of programmatic ads. As more guaranteed placements can be transacted through programmatic pipes, this could bring more efficiency and effectiveness to political marketers, especially for CTV. And as marketers approach signal loss, now is the time to evaluate the solutions that overcome that challenge such as ID alternatives, contextual targeting and geopolitical targeting.

~~~

Basis Technologies has been trusted by agencies and consultants in politics, public affairs, and advocacy for over 15 years. Its Basis platform provides a comprehensive selection of unique buying methods across all channels and devices, utilizing all major creative types and formats. Basis Technologies offers flexible service models with expertise in ad buying tactics for programmatic, vendor-direct, search, and social. Since 2007, Basis Technologies has helped power digital media for over 2,500 political campaigns and independent expenditure committees, and over 2,500 issue advocacy advertisers. Basis Technologies is headquartered in Chicago with 44 offices covering North America, South America and Europe, including a Washington, DC, hub for its Candidates + Causes team.